When it comes to achieving success , whether in finance, business, or personal development setting clear and actionable goals is key. But it’s not enough to just set goals; you need a proven system to actually follow through.

What is Goal Setting?

Goal setting is the process of identifying something you want to achieve and breaking it down into actionable steps. Without clear goals, it’s easy to lose focus and get sidetracked, especially when life throws distractions your way.

In the context of finance and business, goal setting is vital. It gives you direction, keeps you motivated, and provides a measurable path to success. When you know exactly what you want, you’re better able to align your time, energy, and resources toward achieving those objectives.

Why is Goal Setting Important?

Setting goals gives you direction, focus, and motivation — three things that are essential if you want to achieve anything meaningful.

1. Gives You a Clear Sense of Direction

When you set a goal, you define where you’re headed.

Instead of being busy but not productive, every action you take has purpose and meaning.

Example: Instead of “saving money someday” a clear goal might be “save $10,000 for an investment property within 12 months.”

2. Boosts Motivation and Commitment

Goals light a fire inside you. They give you something exciting to work toward and help you push through challenges.

Research by Dr. Edwin Locke, a pioneer in goal-setting theory, shows that people who set specific and challenging goals outperform those who don’t set goals at all (Locke & Latham, 2002).

3. Helps You Measure Progress

When you have clear goals, you can track your progress and see how far you’ve come — which keeps you motivated and helps you adjust strategies when necessary.

4. Sharpens Your Focus

Goals help you prioritize what really matters, so you don’t waste time on distractions.

In finance, for example, setting goals around savings, investments, and debt reduction ensures you build real wealth — not just spend without a plan.

5. Builds Confidence and Momentum

Every time you achieve a goal, big or small, you build self-confidence and momentum.

Achieving one goal fuels the belief that you can achieve the next creating a positive, unstoppable cycle.

The 3 Most Effective Goal-Setting Methods

Let’s explore three proven goal-setting methods that will boost your productivity and increase your chances of success: SMART Goals, Time-Blocking, and the Eisenhower Matrix.

1. SMART Goals

SMART is an acronym that helps ensure your goals are clearly defined and achievable.

- Specific: Your goal should be clear and well-defined.

- Measurable: You need to track your progress.

- Achievable: The goal should be realistic and attainable.

- Relevant: Your goal should matter to your life or business.

- Time-bound: You need a deadline or timeframe for completion.

Example: Let’s say you want to save more money. A vague goal might be, “I want to save money.”

A SMART goal would be:

“I will save $5,000 for an emergency fund by the end of 6 months by setting aside $200 each week from my paycheck.”

This goal is specific (saving $5,000), measurable (trackable with weekly savings), achievable (within your control), relevant (important for financial security), and time-bound (6 months).

2. Time-Blocking

Time-blocking is a method where you schedule blocks of time for specific tasks, ensuring that you stay focused and productive throughout the day.

How to Use Time-Blocking:

- Identify key tasks: Start by identifying all the tasks you need to complete for the day or week. These could be anything from managing your finances, preparing reports, or even personal goals like exercise.

- Create time blocks: Assign specific time slots for each task. For example, allocate 9–11 AM for focused work on financial planning, 1–2 PM for client calls, and 3–4 PM for reviewing your investment portfolio.

- Stick to the schedule: During each block, only focus on the task at hand, no distractions allowed. This maximizes productivity and ensures that you’re making progress on your goals.

Example:

You’ve set a SMART goal to read 3 finance books by the end of the month. By using time-blocking, you might dedicate 30 minutes every morning from 7:00 AM to 7:30 AM to read a chapter. By sticking to this schedule, you ensure consistent progress toward your goal.

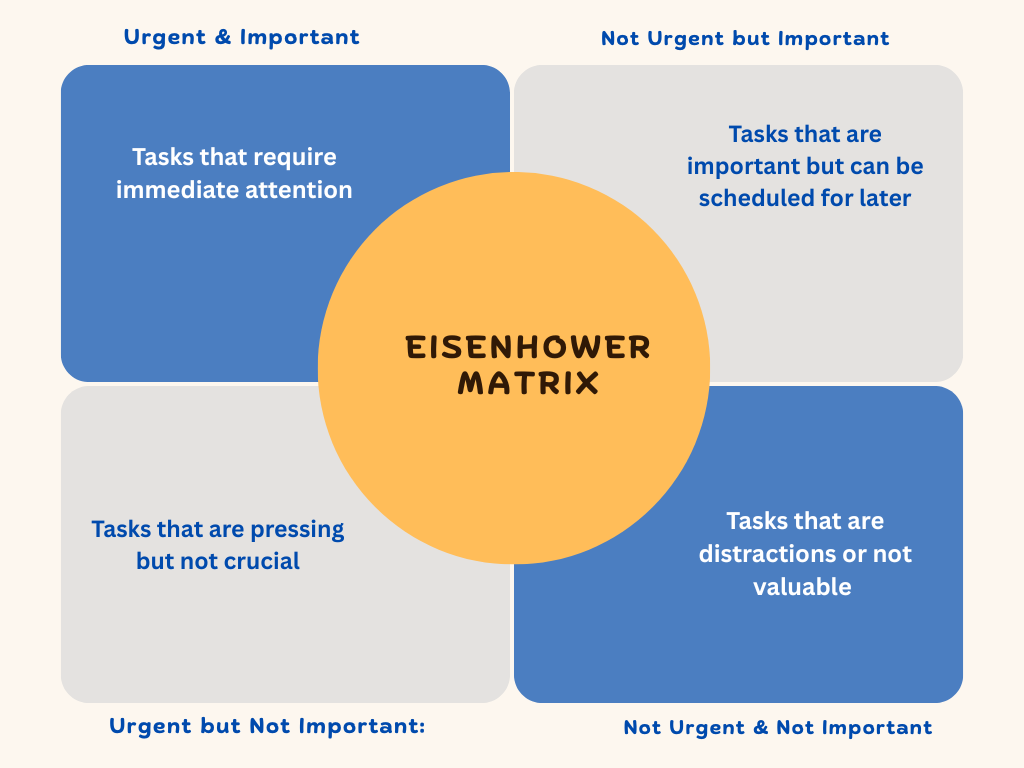

3. The Eisenhower Matrix

The Eisenhower Matrix is a prioritization tool that helps you decide which tasks to focus on first, based on urgency and importance. It divides tasks into four quadrants:

- Urgent & Important: Tasks that require immediate attention (e.g., paying bills, handling urgent business matters).

- Not Urgent but Important: Tasks that are important but can be scheduled for later (e.g., setting up long-term investments, planning your career).

- Urgent but Not Important: Tasks that are pressing but not crucial (e.g., answering non-essential emails).

- Not Urgent & Not Important: Tasks that are distractions or not valuable (e.g., mindlessly scrolling through social media).

How to Use the Eisenhower Matrix:

- List all your tasks.

- Categorize them into the four quadrants.

- Focus on urgent and important tasks first. Delegate or schedule non-essential tasks.

Example:

If you’re a business owner, managing cash flow might fall into the Urgent & Important quadrant, while planning a new product launch could fall under Not Urgent but Important. By focusing your energy where it’s most needed, you ensure long-term productivity and success.

Putting It All Together: A Practical Example

Let’s tie everything together with a practical example. Imagine you’re a financial planner with a goal of increasing your client base by 20% over the next 6 months. Here’s how you could apply the three systems:

- Set a SMART Goal:

“I will increase my client base by 20% in 6 months by reaching out to 5 potential clients every week and attending 2 networking events per month.” - Use Time-Blocking:

Dedicate specific hours each week to client outreach.

- Monday 9–10 AM: Make outreach calls.

- Wednesday 1–2 PM: Attend networking events (or plan them virtually).

By setting aside focused time for each task, you ensure consistent progress.

- Apply the Eisenhower Matrix:

- Urgent & Important: Respond to potential client emails.

- Not Urgent but Important: Create a marketing strategy for future client growth.

- Urgent but Not Important: Answer non-critical admin emails.

- Not Urgent & Not Important: Scroll through social media for personal use.

Why This Matters for Your Financial Success

By setting clear goals and sticking to structured productivity systems, you gain clarity on what needs to be done. This is especially important in finance, where discipline and consistent action lead to long-term wealth.

Without proper goal setting and time management, it’s easy to get distracted by the day-to-day hustle or get overwhelmed by the complexity of financial planning. But by applying SMART goals, time-blocking, and the Eisenhower Matrix, you will build a more productive, focused, and successful path to achieving your financial and business objectives.

Final Thoughts

Setting meaningful goals is the first step to success, but following through is what separates those who achieve greatness from those who don’t.

By using SMART goals, time-blocking, and the Eisenhower Matrix, you’ll not only set the right goals but stay on track to make them a reality.

Remember, every great accomplishment, whether it’s financial freedom, career success, or personal development, begins with a clear goal and a focused plan of action. So, get started today and start turning your goals into reality!